What forms of Opposite Mortgage loans Come?

What is the minimum years requirement for an opposing mortgage? Constantly, 62. But before you have made this sort of financing, find out about the risks, and believe other choices.

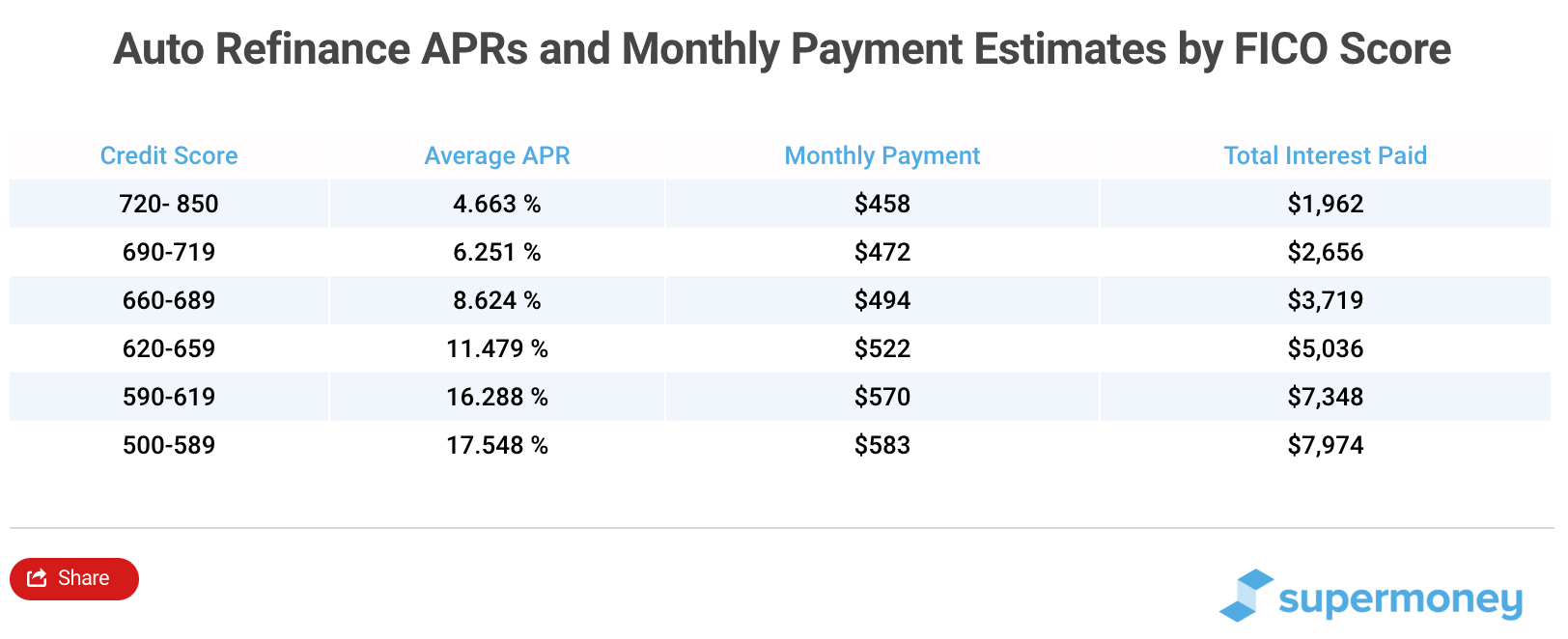

best personal loan lenders in Oakwood

Reverse mortgages are usually claimed given that a good way for the money-secured elderly people and senior citizens locate spending-money instead having to stop their homes. Constantly, minimal age to own requisite an opposing home loan was 62. In some instances, you will be able to find that when you’re more youthful, instance, once turning 55.

But they are such mortgages all of that higher? Contrary mortgages was difficult, high-risk, and you can expensive. Plus of numerous situations, the lending company can be foreclose. Bringing a reverse home loan constantly is not wise, even although you meet with the minimum decades requirement.

Exactly how Opposite Mortgages Works

Which have an opposing financial, you are taking away that loan against the equity of your property. In place of which have a typical home loan, the lending company makes repayments to you that have a contrary financial.

The loan should be paid down once you perish, disperse, import label, or promote the house. But not, for those who violation the newest regards to the loan price, the lending company might telephone call the borrowed funds owed before.

And if you never pay the borrowed funds as the financial accelerates they, you could potentially eradicate the house or property to a property foreclosure.

Household Collateral Conversion process Mortgages

This new Government Property Management (FHA) assures HECMs. Which insurance coverage benefits the lending company, not the fresh homeowner. The insurance coverage kicks from inside the in the event that debtor non-payments towards the mortgage and household isn’t really value sufficient to pay back the lending company entirely as a result of a property foreclosure deals or any other liquidation techniques. The FHA compensates the lender into loss.

To acquire good HECM, you must see strict standards having approval, and additionally the very least decades requirement. You could potentially found HECM payments into the a lump sum (subject to certain limitations), given that monthly installments, once the a credit line, or because a variety of monthly payments and a type of credit.

Exclusive Opposite Mortgage loans

Proprietary opposite mortgage loans aren’t federally covered. This kind of reverse financial might be an effective “jumbo opposite mortgage” (merely people with very high-worthy of land can get him or her) or any other kind of contrary financial, such as for example one geared towards some one ages 55 as well as over.

Other sorts of Opposite Mortgage loans

A different sort of reverse mortgage are a good “single-use” reverse home loan, which is also named a beneficial “deferred commission loan.” This type of contrary mortgage is a desire-created loan for a different sort of purpose, such as for example investing property taxation otherwise paying for household solutions.

Opposite Financial Decades Requirements and you will Qualifications

Once again, the minimum ages need for an effective HECM opposite home loan is actually 62. There is absolutely no top age restriction to acquire an effective HECM contrary financial.

Contrary mortgages do not have borrowing otherwise money criteria. The quantity you might use lies in their residence’s value, newest interest levels, along with your many years. Plus, simply how much of one’s residence’s really worth you can extract are restricted. As of 2022, the quintessential money provided with a HECM is actually $970,800. Along with, a borrower could get only 60% of your mortgage in the closure or perhaps in the initial 12 months, at the mercy of several conditions.

- You must inhabit the property since your dominant home.

- You really must have good-sized guarantee on the possessions otherwise very own the brand new home downright (definition, you don’t have a home loan involved).

- You cannot be outstanding to your a federal debt, such government taxes otherwise federal figuratively speaking.

- You ought to have financial resources available to spend constant possessions can cost you, such as for example house fix, possessions taxation, and you may homeowners’ insurance.

- Your house need to be from inside the good shape.

- The house should be an eligible property form of, such as for instance one-house.